s******m

发帖数: 118 | 1 Please send application and resume to c***********[email protected]

Job Summary:

Assist the Credit Portfolio Management team in managing various projects

to improve portfolio and risk management, including topics such as

Economic Capital (EC), concentration risk management, stress testing,

and portfolio management and hedging. This will include deal risk

adjusted return analysis, deal impact analysis, portfolio optimization

analysis, concentration risk management, credit portfolio hedging,

scenario a... 阅读全帖 |

|

u********e

发帖数: 4950 | 2 ☆─────────────────────────────────────☆

updownlife (渔夫) 于 (Sat May 7 19:23:03 2011, 美东) 提到:

第一届(4/8-4/22)比赛结果: 金牛-JustInCase (28.29%) 银牛-firecs(5.59%) 铜牛-

mikejackson(3.32) 同期SPX(0.69%)

第二届(4/22-5/6)比赛结果: 金牛-alonerocky (6.04%) 银牛-JustinCase(5.16%) 铜

牛-rim

(2.38%) 同期SPX(0.21%)

-------------------------------------------------------------------------

第三届(5/6-5/20)比赛参赛portfolio

-----------------------------------------------------------

Name Stock Selections

alonerocky ... 阅读全帖 |

|

s******m

发帖数: 118 | 3 【 以下文字转载自 JobMarket 讨论区 】

发信人: springmm (new), 信区: JobMarket

标 题: [Job opening] Credit Portfolio Analytics Manager

发信站: BBS 未名空间站 (Mon May 2 18:00:01 2011, 美东)

Please send application and resume to c***********[email protected]

Job Summary:

Assist the Credit Portfolio Management team in managing various projects

to improve portfolio and risk management, including topics such as

Economic Capital (EC), concentration risk management, stress testing,

and portfolio management and hedging. This will incl... 阅读全帖 |

|

u********e

发帖数: 4950 | 4 ☆─────────────────────────────────────☆

updownlife (渔夫) 于 (Mon Apr 25 09:01:16 2011, 美东) 提到:

参赛portfolios:

-----------------------

Name Stock Selections

-----------------------

JustinCase(上届比赛冠军) ANIK VRTX FCSC ANX PATH

firecs(上届比赛亚军) AGU LVS CLF ALU MOS

rotone(上届比赛第四名) DECK COH F WFC TEVA

boshihou2 SINA SOHU TSLA F ZIXI

fei PAY ZIP ARMH POT FSLR

jiangnanhao BIDU IMAX LAVA HW BRKR

al... 阅读全帖 |

|

W********i

发帖数: 1115 | 5 请各位仔细阅读JD再投简历,谢谢。

简单说:

1.给CITI自己的投资相关部门做固定收益和外汇交易衍生品的核算相关的工作。不面对

客户,属于buy side的支持职能。

2.6年工作经验的要求也没有那么硬性了,但起码也得有4年相关工作经验。本科学历

就行,master也可以。

3.纽约,下城,打算长期在美国的, 再考虑。 想随便干干,存点经验就走人的,请绕

行。

4.职位根据实际情况定,基本是AVP或VP

回我公司信箱c********[email protected]

Job Description

Brief Description of the Organization The Global Function units at Citi

include Audit & Risk Review, Compliance, Control & Emerging Risk, AML, Citi

Security and Investigative Services (CSIS), Finance, Strategy, M&A, Investor

Relations, Global Public Aff... 阅读全帖 |

|

c*y

发帖数: 137 | 6 We are a global equities team in a large hedge fund with offices in both

Stamford and NYC, and we are looking to hire an equity portfolio

optimization intern/consultant to work on our new portfolio optimization

platform. The position is located in midtown NYC; compensation depends on

your level of experiences.

Please submit your resume to : c**[email protected] or apply through the

following URL:

https://careers.sac.com/JobDetail.aspx?id=150

Job Title: Portfolio Optimization Specialist Int... 阅读全帖 |

|

c*y

发帖数: 137 | 7 For some reason, my earlier post was deleted from this board, so I am

posting it again. We have received some strong resumes and will be

conducting phone interviews from next week. If you have strong background in

optimization theories, please submit your resume to c_yy@

hotmail.com or apply through the following URL:

https://careers.sac.com/JobDetail.aspx?id=150

BTW: If you could list your past experiences/projects/research/publications

in the area of numeric analyses and optimizations, it woul... 阅读全帖 |

|

c*y

发帖数: 137 | 8 For some reason, my earlier post was deleted from this board, so I am

posting it again. We have received some strong resumes and will be

conducting phone interviews from next week. If you have strong background in

optimization theories, please submit your resume to c_yy@

hotmail.com or apply through the following URL:

https://careers.sac.com/JobDetail.aspx?id=150

BTW: If you could list your past experiences/projects/research/publications

in the area of numeric analyses and optimizations, it woul... 阅读全帖 |

|

w*******y

发帖数: 60932 | 9 i say bet on gold

Link:

http://www.cnbc.com/id/44207374/CNBC_S_MILLION_DOLLAR_PORTFOLIO

NO RISK. ALL REWARD. GRAND PRIZE: $1 MILLION

Registration for the ten-week, global fantasy stock and currency trading

competition opens today

ENGLEWOOD CLIFFS, N.J., Aug. 22, 2011 -- What would you do if you had a

million dollars? Would you buy something? Invest it? Give it away? Starting

today, all aspiring millionaires can register to try their hand at managing

a $1 million "CNBC Bucks" stock & currency por... 阅读全帖 |

|

u********e

发帖数: 4950 | 10 (5) 奖励规则:

* Highest return portfolio 获 金牛奖 (奖金400伪币)

* Second high return portfolio 获 银牛奖 (奖金200伪币)

* Third high return portfolio 获 铜牛奖 (奖金150伪币)

* 其他 top 10 beat S&P500 的portfolio 将获大牛奖 (马克,总奖金20伪

币)

* 分析奖: 带分析(TA 或 FA) 参赛并获上述牛奖的portfolio 可以并获大牛分析

奖(马克痣腚并另加奖金10伪币,总额外奖金20伪币)

* 超级大牛奖: 每次比赛捐款和除去手续费150伪币之后未分配盈余将累计后奖励连

续2次进入top 3 的超级大牛 (每次超级大牛奖金: 500 伪币)

* 大牛入场奖:连续2次进入top3 的大牛在参加第3次比赛时将获得 10 个包子(100

位比)大牛入场奖

(6) 报名人数和办法:

* 每次比赛接受30个portfolio

* 上届比赛top 3 选手可以有直接进入下届比赛

* 其他27名按 first come fir... 阅读全帖 |

|

L*******t

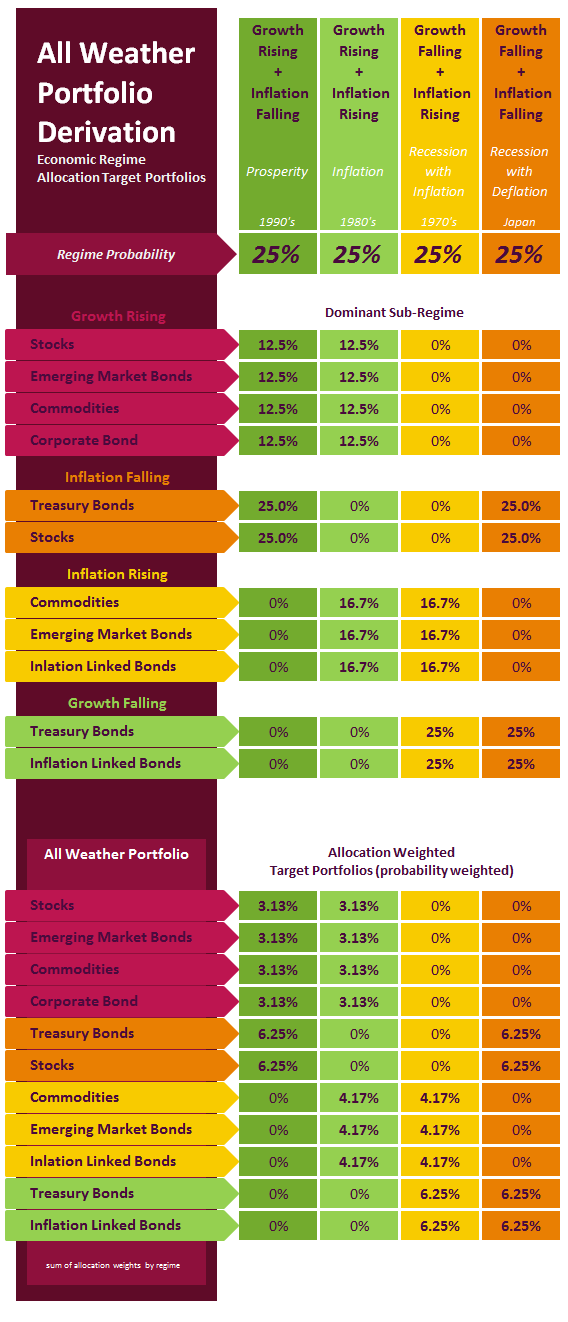

发帖数: 2385 | 11 看到一篇文章,觉得挺不错的,不知道是不是too old

全文如下。

The new portfolio management view is that the focus of investors should be

on risk-based investment decisions not asset-based decisions. Stop thinking

about what is your exposure to bonds or stocks and think about your exposure

to inflation or economic growth. The assets do not matter. The factor risks

matter.

It is not easy to make this switch and it still requires that you map risks

into asset allocation space, but this focus on factor risks is a strong

advanc... 阅读全帖 |

|

w**k

发帖数: 6722 | 12 亏废了

And now I know my portfolio is a ghost town

My portfolio is a ghost town

My portfolio is a ghost town

My portfolio is a ghost town

There's no green left in the world

I'm bag-holding'

Don't give a damn if I go

Down, down, down

I got a ticker in my head that keeps singing

Oh, my portfolio is a ghost town

求包子安慰 |

|

发帖数: 1 | 13 本人数学专业,有两个学生在我班里上过四门课,每门课都是A。我觉得他们还是挺喜

欢我的teaching style的, 因为我并不是放水换好评的。交tenure 材料的话,找个学

生说两句好评放在portfolio里合适吗?也未必是推荐信的正式形式了,写上一两段对

我教学的评价。

现在不确定联系他们,把评语email发给我好,还是发给系主任好?还是这种评语一点

分量没有,不需要加到portfolio里?

还有个问题,打算加一些以前的final或quiz什么的在portfolio里,空白的好,还是选

一些学生的final exam,把名字抹去比较好?这些都是不要求的,只是想让case看起来

更强一点。各位已经tenure的给点意见,什么optional的材料加到portfolio里比较好

?谢谢! |

|

b****n

发帖数: 993 | 14 Permanent portfolio是一个不错的方法,虽然严格执行的时候会有困难:因为它和市

场之间的tracking error有时候会很大,很多人可能会坚持不下去。

这里有篇文章讨论了一个permanent portfolio fund:PRPFX。这个基金的问题之一就

在于有点随意地偏离permanent portfolio主张的asset allocation,结果是不太妙,

16年平均下来每年比严格的permanent portfolio低一个百分点,而风险则高两个百分

点。

http://www.efficientfrontier.com/ef/0adhoc/harry.htm

back |

|

k*****k

发帖数: 78 | 15 我朋友是财务顾问,她建议我在401K里100%投到 American Century One Choice 2045

Portfolio Fund (ARORX) ,但是我看了YTD Return 似乎并不理想,背后的理由是什么?

我是菜鸟,谢谢各位指导啦!

American Funds Balanced Fund (RLBBX) 12.25%

American Century One Choice 2045 Portfolio Fund (ARORX) 11.75%

American Century One Choice 2050 Portfolio Fund (ARFWX) 12.06%

Select Fndmntl Val Fd (Wellington) (MFUAX) 22.07%

Mutual Financial Services Fund (TFSIX) 16.35%

Select Focused Value Fund (Harris) (MFVAX) 23.53%

MM S&P 500 Index Fund (MIEAX) ... 阅读全帖 |

|

c******z

发帖数: 1230 | 16 用SigFig汇总了几个brokerage账户里的portfolio,每周SigFig会发一个email简报,

会列出我的portfolio和S&P500/DJIA同期的performance,每次看到email都不开心啊。

。。。

下面是最新收到的简报,我的portfolio的绝大部分还是Schwab的Managed Account,他

们给的组合且进行管理的,但1year和YTD的收益才是S&P500的一半。我应该这么比较吗

?应该退出Schwab的组合,重新调整吗?

Portfolio's Performance

1 week 1 month 3 month 1 year YTD

You -0.3% -5.4% -4.0% 3.8% 1.2%

DJIA -1.0% -5.2% -4.2% 6.4% -1.2%

S&P 500 -1.0% -6.2% -4.6% 8.2% ... 阅读全帖 |

|

y*******d

发帖数: 1674 | 17 对于投资小白,那种问几个问题,然后给你免费建portfolio的网站好么?

比如Schwab

Who has time to manage their portfolio like a pro?

You do. With $5,000 to invest, Schwab Intelligent Portfolios™

sophisticated technology will build, monitor and rebalance a diversified

portfolio based on your investment goals. Enrollment is easy with just a few

straightforward questions. Plus, there are no advisory fees, commissions or

account service fees charged. |

|

m****d

发帖数: 331 | 18 risk-neutral probabilities: q_i,

real-world probabilities: p_i

let c=dQ/dP which is a vector with entires c_i=q_i/p_i

Let x be the portfolio that replicates c.

what does "Let x be the portfolio that replicates c." mean?

anything related to market portfolio?

I know that if a portfolio can be replicated, it means that Ax=y can be

solved, where A is the payoff matrix. Thanks. |

|

B*******t

发帖数: 135 | 19 有两个portfolios:P1和P2。他们的1day的5%的VaR分别是2m和3m,

那么把这两个portfolio合起来作为一个大的porfolio来考虑,大portfolio的1day 5%

的VaR是多少?

好像这个问题还挺复杂的。两个portfolio的价值,V1和V2。如果仅仅知道 DeltaV1和

DeltaV2的correlation,可以得到最终答案么?还是说必须DeltaV1和DeltaV2的joint-

distribution?

先提前谢谢大牛们指教了! |

|

w*******y

发帖数: 60932 | 20 Craftsman 9 x 11 in. Sandpaper 50-pk with Storage Portfolio - $8.07 @ Sears

Click Here first to activate the 5% off

Craftsman 9 x 11 in. Sandpaper 50-pk with Portfolio:

http://www.sears.com/shc/s/p_10153_12605_00922893000P

[sears.com]

an additional 15% comes of in your cart

Extra 15% off select tools! Applies to items Sold by Sears. Offer valid 5/20

- 5/21

Earn 2X points! 20 points per $1 spent on Tools sold by Sears. Offer ends 5/

21/11. Offer ends 21-May-2011.

Select pick up in store to save o... 阅读全帖 |

|

m***e

发帖数: 428 | 21 I just chaired a committee to evaluate teaching portfolios of nontenured

faculty members. They include materials such as syllabus, exams,

assignments, guidelines for writing term papers for all courses most

recently taught. Whether teaching evaluations are included in teaching

portfolio may depend on the specific university. Actually in my university,

students' evaluations are not part of teaching portfolio. |

|

O***C

发帖数: 1219 | 22 我有10几只ETF和10几只股票(大约一半美股,一半中概),希望Portfolio功能较强。

能够按当天收市价显示出我的投资组合在不同地区,不同行业中所占的比重。

MORNINGSTAR的Portfolio可以做到这一点。

但是我还希望它能把我持有的ETF按照权重拆分成一只只股票,和我持有的股票叠加在

一起,排列出我的投资组合在每只股票上所占的比重。

MORNINGSTAR要求只有高级会员才能享受这项服务,而我的试用期结束了。

请问Google,Yahoo的Portfolio功能如何?能做到这一点么?

如果不能,什么网站能做到这一点?

谢谢指教! |

|

m**********r

发帖数: 887 | 23 Follow the permanent portfolio strategy, you do not need to adjust your

portfolio very often.

start from:

25% cash

25% 20 year+ treasury bond

25% total market equity fund

25% gold

when one sector grow beyond 35% or fall below 15% adjust the portfolio back

to 25/25/25/25 |

|

|

c******z

发帖数: 1230 | 25 预约了Fidelity local office的VP要面谈,咨询managed brokerage account。

初步电话咨询了解到,他们的服务叫Fidelity Portfolio Advisory Service,貌似和

其他公司的账户的不同之处在于:这个Service下面可以有多个、不同种类(Tax-

sheltered, general inverstment, etc.)、不同管理方法(Taxsensitive, etc.)的

账户,不过应该都是discretionary account.

年管理费Between 0.25% and 1.7% of your eligible assets invested。资产超过

250K会配一个Account Executive和一个dedicated Portfolio Specialist.

他们的网页介绍如下,https://www.fidelity.com/managed-accounts/portfolio-

advisory-service

这样的账户应该比自己啥也不懂、随便卖要安全一些吧?请大家指点有没有啥缺陷、陷

... 阅读全帖 |

|

|

S*******s

发帖数: 13043 | 27 谁研究过IB在portfolio margin和regular T下计算margin的区别?我转到portfolio

margin以后居然margin变大了。什么样的组合更适合在portfolio margin下? |

|

m******8

发帖数: 1676 | 28 我刚才看了一下, 你如果有几个PORTFOLIO 在里面,

点“PORTFLIOS”, 显示所有的PORTFOLIO, 但DAYS GAIN, TOTAL GAIN 的% 没除100.

这YHOO 什么水平? |

|

发帖数: 1 | 29 Portfolio lender 一般会自己hold loan,不卖给二级市场,因而利率也会偏高。一般

要送portfolio Lender 可能是房子有一些特殊情况不能满足Fannie Mae和Freddie Mac

的要求.

如果有问题可以直接联系我。联系方式发到您站内信了。

谢谢!

portfolio

just |

|

O*******d

发帖数: 20343 | 30 portfolio本意是皮包,转意成一套资料的意思。 在不同的语境有不同的翻译。

投资的portfolio是你全套投资的资金分布,例如多少股票,多少基金。

摄影师的portfolio是他的全套摄影作品。 |

|

B*********h

发帖数: 800 | 31 ☆─────────────────────────────────────☆

nikki0202 (nikki) 于 (Tue Mar 13 01:21:21 2007) 提到:

IB得portfolio manager和trader,是同一种职位马?

☆─────────────────────────────────────☆

kongkongj (happyhappy) 于 (Tue Mar 13 01:44:29 2007) 提到:

portfolio manager一般是buy side firm用的title?哪位大牛给详细讲讲啊,同问

☆─────────────────────────────────────☆

datouzhu (datouzhu) 于 (Tue Mar 13 09:54:43 2007) 提到:

portfolio manager and prop trader are buy-side. Genereal term "trader"

ususally refer ro sell-side trader.

☆──── |

|

B*********h

发帖数: 800 | 32 ☆─────────────────────────────────────☆

KuangTer (KuangTer=Quant) 于 (Sun Mar 18 15:07:29 2007) 提到:

I do not know a lot of quantitative portfolio management except some game-

level little projects in my optimization method in finance course. I

remember that the faculty also told us the optimization method in portfolio

management is not robust. I wonder if the quantitative portfolio management

similar with optimization in finance and is it a promising job if I really

like quantitative modelin |

|

d******n

发帖数: 4 | 33 不知道这个贴发在quant版是否合适,但是希望斑竹手下留情吧。

我将去一个interview, 是关于quantitative portfolio management 的工作,fixed

income。

先说说我的背景,recent Engineering PhD,可是我一直都在准备quant,对于portfolio

management不是很熟悉,除了学了一些基本的知识如market portfolio, sharp ratio

.

请问有经验的朋友可否提点一下,这类面试中一般的问题大概涉及什么方面的知识?

谢谢。 |

|

k**u

发帖数: 698 | 34 【 以下文字转载自 Trading_System 俱乐部 】

发信人: liliwater (lyrist), 信区: Trading_System

标 题: Portfolio optimization

发信站: BBS 未名空间站 (Thu Feb 11 21:17:33 2010, 美东)

method:Mean-CVaR

portfolio : 30 stocks in DJI over past 10 years

benchmark : a modified DJI

strategy : long only and long/short

rebalance : monthly

transaction fee : not considered

results:

long only:

Net Performance % to 2010-02-28:

1 mth 3 mths 6 mths 1 yr 3 yrs 5 yrs 3 yrs p.a. 5 yrs p.a.

Portfolio 0.04 -1.84 5.05 24.74 -3.98 23.8 |

|

q*******t

发帖数: 17 | 35 http://www.quantspot.com/jobs/list/18878-Shanghai-Quantitative-Analyst-(Portfolio-Analysis)

The "Portfolio Analysis and Tools" team is responsible for

analyzing the performance of large asset portfolios

automating processes that combine data and model into analysis engines and

providing the front desk with timely and handy tools for pre- or post-trade

analysis.

Requirements

Our ideal candidate should have the following credentials or skills:

Master/PhD degree in Finance, Math, Physics, Engineeri |

|

k**k

发帖数: 61 | 36 大家好,请教个问题。

已有一组simulated returns of constituent stocks (20*10000,即20个stock,共

10000组correlated returns)。想在某个portfolio target return的constraint下通

过变化stock weights来minimize portfolio expected shortfall,不知道该如何设

objective function。主要是如何将每个scenario下portfolio expected shortfall的

计算直接体现在objective function中不知道如何处理。optimization打算直接用

fmincon函数做。大家有什么建议没有? |

|

V******t

发帖数: 35 | 37 Job positions from CITIC Securities are open to overseas candidates.

Interested candidates please send a copy of your resume to:Luo, Lin at luol@

citics.com

Department: Equities & Derivatives Trading.

Position: Director or Senior Vice President (China/International multi-

strategy proprietary trading)

Number: 10

Location: Beijing or Hongkong

Preferred strategies: High frequency trading, Statistical arbitrage, Market

neutral, CTA trading, Equity long/short, Convertible arbitrage and Event

drive... 阅读全帖 |

|

o********n

发帖数: 100 | 38 小弟现在在给一家公司开发交易策略。 目前问题是整合自有策略到mean-variance

portfolio下时,发现简单的mean-variance portfolio的表现非常差。怀疑要嘛是

estimation of covariance structure 结构有问题,要嘛是代码有问题。

想请教一下有经验的朋友, 一般portfolio selection的测试数据,会如何生成? 一

般需要考虑哪些情况?

谢谢! |

|

k****e

发帖数: 23 | 39 portfolio由两个stock (A, B)组成, 以下是信息:

arithmetic mean return: Ra Rb

geometric mean return: Ga Gb

standard deviation: Ta Tb

Correlation: p

Weight: Wa, Wb

Portfolio arithmetic mean return = Ra * Wa + Rb * Wb

请问: 怎么算 Portfolio geometric mean return? |

|

w*******y

发帖数: 60932 | 40 Click Here first to activate the 5% off

Craftsman 9 x 11 in. Sandpaper 50-pk with Portfolio:

http://www.sears.com/shc/s/p_10153_12605_00922893000P

an additional 15% comes of in your cart

Select pick up in store to save on shipping

Final Price $8.07

Product Description

50-pack of Craftsman 9 x 11 in. Aluminum oxide sandpaper. This General-

purpose sandpaper is ideal for hardwoods, metal and fiberglass; the durable

synthetic material has self-renewing properties that breakdown under the

heat and... 阅读全帖 |

|

w*******y

发帖数: 60932 | 41 Portfolio Stainless Steel Solar-Powered LED Path Lights Buy 2 get 1 free. $6

.68 for 3. Free Store Pickup from Lowe's

Add 2 to cart, 3rd one will be added to cart automatically

Portfolio Stainless Steel Solar-Powered LED Path Light:

http://www.lowes.com/pd_335634-59179-MS16MA-N2-SS-T25_429478977 Hero Special Values

3 for $6.68

Other Buy 2 get 1 free Portfolio Solar Lights:

http://www.lowes.com/pl_Lighting Hero Special Values_4294789770_4294937087_?cm_mmc=email_promo-_-20110519_V2-_-product_2-_-... 阅读全帖 |

|

w*******y

发帖数: 60932 | 42 Craftsman 9 x 11 in. Sandpaper 50-pk with Portfolio:

http://www.sears.com/shc/s/p_10153_12605_00922893000P

- $8.09

Select Pick up in store to save on shipping

Product Description

50-pack of Craftsman 9 x 11 in. Aluminum oxide sandpaper. This General-

purpose sandpaper is ideal for hardwoods, metal and fiberglass; the durable

synthetic material has self-renewing properties that breakdown under the

heat and pressure of continuous sanding to create new sharp edges. Aluminum

oxide grit for general... 阅读全帖 |

|

m**********r

发帖数: 887 | 43 ”This portfolio is a half-step away from a cellar-full of canned goods and nine-millimeter rounds,”

【 以下文字转载自 Investment 讨论区 】

发信人: mygoldfinger (金手指), 信区: Investment

标 题: Ron Paul's personal investment portfolio

发信站: BBS 未名空间站 (Fri Jan 6 09:17:10 2012, 美东)

According to Wall Street Journal

http://blogs.wsj.com/totalreturn/2011/12/21/the-ron-paul-portfo

He owns no bonds or bond funds and has only 0.1% in stock funds. Furthermore

, the stock funds that Rep. Paul does own are all “short,” or make... 阅读全帖 |

|

a***e

发帖数: 38850 | 44 我不讲故事, 我只讲事实和证据。

1)

5/9/12 A的信

“活神,你好,我现在手上有如下物品,查了下二手好像都是你在收的

1. HP P1606DN 四台

2. canon ehpl100 一个,颜色:gray

3. canon sx150 一个,颜色: black

请问你说吗?

另外我想请问下,我今年11月中以后会回国较长一段时间 ,所以如果这几个东西你收

的话,你有可能在这之前尽量让我把货发完吗?

多谢!

不好意思,上封信把两个相机的颜色写反了。

”

没说任何labelready的事。

2)

我同时回复她 staples还有deal,她的5/9/12回复:

“多谢活神提供的deal信息,我这周已经买了1606DN了,几个离得近点的店子都露过面

了,不想让小二印象太深刻,所以还不确定去不去买其他的几种打印机,要是去买到了

再和你联系吧,目前就暂定出买到的这些好了。

再次多谢!”

显然deal还活着, 我不可能label ready。

请问portfolio的label ready的story从哪里编的???

中间7/9/12出动掉elph 100.7/9/12 email:

... 阅读全帖 |

|

n******r

发帖数: 294 | 45 tenure材料一般学校都包含professional essay,就是自己教学科研服务上的成就和心

得体会。我在essay里教学的部分引用了几句学生的评语,都是从学生反馈里挑的。我

觉得学生评语放在portfolio里没问题,但应该出自学生期末反馈才有说服力,因为是

匿名的。直接向学生要推荐信不合适,因为作为教师你处于authority的位置,向学生

要推荐信会给人以学生迫于压力说好话的感觉。

加一些以前的final或quiz什么的在portfolio里没问题,不过这些东西一般没人会太

care。 |

|

t***s

发帖数: 163 | 46 【 以下文字转载自 Quant 讨论区 】

发信人: meever (Life\\\\\\\'s a struggle), 信区: Quant

标 题: 苦闷, portfolio optimization 问题求助

发信站: BBS 未名空间站 (Mon Sep 10 14:44:07 2007)

我是一个学portfolio optimization方面的phd学生. 本来一直对quant很感兴趣, 做了

两年多的research越来越觉得自己没这个天份. 很想请求板上的高人指点指点.

从markowitz到后面一些复杂的方法, 近几年paper里面的我都读了一些, 自己跟着做了

一些, 但是好多我读到的都是很多的理论, 最后的检验却少的可怜, 都是很少的data,

或者很少的几个stock在做. 我自己做的结果更是令我很丧气. 回到最基本的东西, 我

发现历史上的return跟未来的return联系很小, 只有volatility似乎是有联系的, 其它

从mean,到skewness 到kurtosis到很多其它statistics都很难找出联系. 那么大家根据

过去来opti |

|

K****D

发帖数: 30533 | 47 ☆─────────────────────────────────────☆

immortal (immortal) 于 (Mon Sep 22 14:53:19 2008) 提到:

发信人: Nikki2008 (Nikki), 信区: Stock

标 题: 晒晒我的portfolio

发信站: BBS 未名空间站 (Mon Sep 22 13:48:45 2008)

It is not show off post,I am just looking forward hearing your inputs。

1. US stock market:

Net value: 80,599.40 USD

Composition: 80% cash, 20% high tech stocks(JAVA,CSCO,NOK,ORCL)

2. Mutual fund:

FRANKLIN INCOME CLASS C:

Mkt value:8,775 USD

(When I purchased it 2 years ago, it worthed 10,000 USD.)

3. U.S ... 阅读全帖 |

|

K****D

发帖数: 30533 | 48 那样就比较怪了,呵呵。要么是你的FA worked, 要么就是你的portfolio

是bull biased,因为7个月以来A股基本上是牛市。偶本人不是很相信一个

non-active的portfolio可以长期beat index. |

|

s******d

发帖数: 323 | 49 not the fund PRPFX, but the actual portfolio proposed by Harry Browne.

It's such a simple, but unintuitive, but again excellent idea.

the allocation goes like this:

25% gold: economic and political turbulence, unexpected inflation

25% LT treasury bond: deflation, flight to quality

25% cash: recession, expected inflation

25% stocks: prosperity

gold, LT t-bond, cash are all considered bad long term investment ideas,

but together in this portfolio they work beautifully. It will never

get you super |

|

s******d

发帖数: 323 | 50 from 1972-2007, the portfolio returns 10.02% annually without much

volatility.

obviously the portfolio did much better than stocks in 2008.

It won't make you rich overnight, but certainly preserve your purchase power

very well.

who |

|

{kind=link}